Full and Final Settlement is the comprehensive process of calculating and paying all outstanding dues to an employee leaving an organization. These financial dues may include last salary, leave encashment, gratuity, bonuses, commissions, etc. It should be paid to all employees irrespective of their exit mode, such as resignation, termination, or retirement.

FnF goes far beyond the final salary. It is a complete financial reconciliation: the employer clears everything owed to the employee (salary, leave, gratuity, bonus, reimbursements) and recovers everything owed by the employee (notice shortfall, loans, unreturned assets).

In India, FnF is a legally mandated process governed by the Code on Wages 2019, Payment of Gratuity Act 1972, EPF Act 1952, Industrial Disputes Act 1947, and applicable state Shops & Establishment Acts.

FnF full form is Full and Final Settlement. It is also written as F&F settlement, full and final payment, or final settlement. In Indian HR and payroll contexts, all four terms refer to the same process of clearing all financial dues when an employee exits an organisation.

You may also encounter: FnF letter (the settlement statement issued to the employee), FnF calculation (computing the exact amount payable), and FnF process (the step-by-step workflow of completing the settlement).

On November 21, 2025, India brought four consolidated Labour Codes into force, repealing 29 older labour laws. For payroll and HR professionals, the most immediate operational impact is a radically shortened FnF timeline.

“Where an employee has been removed or dismissed from service, or retrenched or has resigned from service, or became unemployed due to closure of the establishment, the wages payable to him shall be paid within two working days of his removal, dismissal, retrenchment or, as the case may be, his resignation.” — Section 17(2), Code on Wages, 2019

This is a fundamental shift. The old industry practice of 30–45 days is no longer legally compliant for wage components. The 2-day rule applies to all employees regardless of salary level, designation, or industry.

What changes: Previously, most companies ran FnF clearances sequentially — IT first, then Finance, then HR, then payment. Under the 2-day mandate, all clearances must run in parallel.

What doesn’t change: Gratuity still follows its own 30-day timeline under the Payment of Gratuity Act 1972. EPF still follows EPFO processes.

| FnF Component | Governing Law | Deadline (2026) |

|---|---|---|

| Wages: salary, leave encashment, bonus, reimbursements | Code on Wages, 2019 — Section 17(2) | 2 working days from last working day |

| Gratuity | Payment of Gratuity Act, 1972 | 30 days from last working day |

| EPF transfer or withdrawal | EPF & MP Act, 1952 + EPFO | 15–20 working days (EPFO) |

| Retrenchment compensation | Industrial Disputes Act, 1947 | On or before last working day |

| Notice pay in lieu of notice | Employment contract terms | On or before last working day |

This is the most underreported change in India’s Labour Codes — and it directly increases gratuity and PF in every FnF calculation.

While the 2-day payment mandate gets all the attention, India’s new Labour Codes introduced a second equally significant change that directly impacts every full and final settlement calculation: the 50% Wage Rule.

Under the Code on Wages 2019 and the Code on Social Security 2020, a new uniform definition of “wages” has been introduced. It mandates that:

Basic Pay + Dearness Allowance (DA) + Retaining Allowance must together form at least 50% of an employee’s total CTC.

If allowances (HRA, special allowance, conveyance, bonus, commissions) exceed 50% of total remuneration, the excess amount is automatically added back to “wages” for all statutory calculations — including PF, gratuity, overtime, and ESIC.

Source: Section 2(y), Code on Wages, 2019 & Code on Social Security, 2020 — labour.gov.in

For years, many Indian companies kept basic salary artificially low — at 30–40% of CTC — to reduce their PF and gratuity liability. That practice is now non-compliant. The 50% Wage Rule forces a restructuring that directly increases the FnF payout for employees in two ways:

| Impact Area | Before 50% Rule (Old Practice) | After 50% Rule (New Compliance) |

|---|---|---|

| Basic salary as % of CTC | 30–40% (common practice) | Minimum 50% (mandatory) |

| Gratuity base | Calculated on lower basic (e.g. ₹20,000) | Calculated on higher wage base (e.g. ₹35,000) |

| Gratuity amount in FnF | Lower payout | 25–50% higher payout for employees with low basic structures |

| PF contribution base | 12% of lower basic | 12% of higher wage base |

| PF corpus at exit | Lower EPF balance | Higher EPF balance — more for employee on exit |

| Fixed-term employee gratuity | Only after 5 years of service | After just 1 year (Code on Social Security 2020) |

Consider an employee with a CTC of Rs. 10,00,000 per year (Rs. 83,333/month) who has served 6 years:

| Scenario | Basic Salary | Gratuity Calculation | Gratuity in FnF |

|---|---|---|---|

| Old structure (basic = 35% of CTC) | Rs. 29,167/month | 29,167 × 15 × 6 ÷ 26 | Rs. 1,00,962 |

| New structure (basic = 50% of CTC — mandatory) | Rs. 41,667/month | 41,667 × 15 × 6 ÷ 26 | Rs. 1,44,232 |

| Increase in gratuity payout to employee | +Rs. 43,270 (+43%) | ||

Replaces the Payment of Wages Act 1936, Minimum Wages Act 1948, Payment of Bonus Act 1965, and Equal Remuneration Act 1976. Section 17(2) mandates FnF wage payment within 2 working days. Applicable to all employees across all industries.

Gratuity is mandatory for employees with 5+ years of continuous service (or 1 year for fixed-term employees under new Labour Codes). Must be paid within 30 days of exit. Forfeit is possible only in cases of wilful omission, damage, or violence under Section 4(6). Tax-exempt up to Rs. 20 lakhs for non-government employees. Read our detailed guide on gratuity calculation in India.

EPF contributions (employee 12% + employer 12% of basic + DA) form part of FnF. On exit: employee can withdraw (if not joining another EPF-covered employer) or transfer. EPS withdrawal only possible if service < 10 years. Processed via EPFO portal. Learn more about EPF and PF withdrawal process.

Governs retrenchment. Establishments with 100+ workers must give 1 month written notice or equivalent pay before retrenchment. Retrenchment compensation: 15 days’ average pay per completed year of service. Source: Ministry of Labour & Employment.

State-specific rules on leave encashment limits, notice period norms, and FnF documentation. Maharashtra Shops & Establishment Act, Karnataka S&E Act, Delhi S&E Act — each has slightly different provisions. Always verify your state’s act.

Governs TDS deduction on taxable FnF components. Form 16 must reflect all FnF payments at year-end. Failure to deduct correct TDS makes the employer liable for the shortfall. Reference: incometaxindia.gov.in.

Salary for the days worked in the final month of employment.

Also includes: unpaid salary arrears, pro-rata annual allowances (LTA, medical reimbursement) calculated to last working day, and pending variable pay.

Unused earned leave / privilege leave accrued can be converted to money on exit. Sick leave and casual leave are generally not encashable. Read our detailed guide on leave encashment calculation and taxation.

Payable to employees with 5+ years of continuous service (4 years 240 days in some court interpretations). See our complete gratuity calculation guide for detailed examples.

Tax: Exempt up to Rs. 20 lakhs for private sector (Section 10(10) of Income Tax Act).

Any pending performance bonus, statutory bonus under the Payment of Bonus Act (for eligible employees with basic ≤ Rs. 21,000/month), or quarterly/annual incentives earned but not yet paid.

All pending claims — travel, medical, telephone, fuel, internet — submitted before the last working day and not yet processed.

If the employer asks the employee to leave immediately without serving notice, the employer must pay the equivalent salary for the notice period waived.

Applicable only when the employee fails to serve the full contractual notice period and the company has a buyout clause in the offer letter.

Outstanding balance of any salary advances or company loans disbursed to the employee.

Cost of unreturned or damaged company assets (laptop, phone, ID card) — only if stipulated in the employment contract and supported by a signed asset acknowledgement.

Tax Deducted at Source on all taxable FnF components at the applicable income tax slab rate.

Applicable in states like Maharashtra, Karnataka, West Bengal — deducted from the final month’s salary components.

Here is a complete, real-world FnF calculation example:

| Component | Formula Applied | Amount (Rs.) |

|---|---|---|

| Pro-rata salary (March) | 90,000 ÷ 26 × 15 days worked | 51,923 |

| Leave encashment | 36,000 ÷ 26 × 22 unused leaves | 30,462 |

| Gratuity (6 years) | 36,000 × 15 × 6 ÷ 26 | 1,24,615 |

| TOTAL EARNINGS (A) | 2,07,000 | |

| (-) Notice period recovery | 90,000 ÷ 30 × 30 days short | (90,000) |

| (-) Outstanding loan | Per loan agreement | (20,000) |

| (-) TDS (estimated) | On taxable salary + leave encashment | (4,200) |

| NET FnF PAYABLE | ₹92,800 | |

| FnF Component | Tax Treatment | Exemption / Limit |

|---|---|---|

| Pro-rata basic salary | Fully taxable | None |

| HRA (last month) | Taxable — exemption under 10(13A) | Subject to HRA exemption formula |

| Leave encashment — resignation (private sector) | Fully taxable | None for private sector on resignation |

| Leave encashment — retirement (private sector) | Partially exempt | Up to Rs. 25 lakhs (Section 10(10AA)) |

| Gratuity — non-government employee | Tax-exempt up to limit | Rs. 20 lakhs (Section 10(10)) |

| Gratuity — government employee | Fully tax-exempt | No limit |

| EPF withdrawal — service < 5 years | Taxable, TDS at 10% | Form 15G/H can avoid TDS if below limit |

| EPF withdrawal — service 5+ years | Fully tax-exempt | Section 10(12) — full exemption |

| Retrenchment compensation | Partially exempt | Rs. 5 lakhs or as notified |

| Notice pay received by employee | Fully taxable | None |

| Bonus / incentive payout | Fully taxable | None |

Most common. FnF includes all standard components. Notice period recovery deducted if full notice not served. Gratuity payable if 5+ years served.

Gratuity can be forfeited under Section 4(6) of the Payment of Gratuity Act in cases of wilful omission, damage to property, or workplace violence. All other components remain payable. Notice pay is not applicable as the employer provides show-cause notice.

Retrenchment compensation: 15 days’ average pay per completed year of service (Industrial Disputes Act 1947). Applicable to establishments with 100+ workers. One month written notice or pay in lieu mandatory. Source: Ministry of Labour & Employment.

Full gratuity payable. Leave encashment at retirement is more tax-favourable — up to Rs. 25 lakhs exempt for private sector. EPF fully tax-exempt with 5+ years.

FnF paid to legal nominee. Full gratuity payable regardless of service years. EPF and EPS nominee claim filed with EPFO.

No gratuity if service < 5 years. Fixed-term employees now eligible for gratuity after just 1 year under new Labour Codes. Leave encashment as per company policy.

This is the section most HR guides skip — and it is one of the most important.

Every employee who exits your organisation carries a story about how you treated them at the end. That story gets told on LinkedIn, Glassdoor, AmbitionBox, and in every future interview where someone asks “Why did you leave your last job?”

Organisations that use automated FnF systems report 40–60% fewer settlement disputes and dramatically faster processing. See how Pocket HRMS automates FnF settlements.

If you are an employee receiving your FnF statement, here is what you must verify before signing:

You are not obligated to sign a FnF statement you disagree with. Raise a written objection with HR. Under the Code on Wages 2019, you have a legal right to the correct amount.

Use this template to formally request your FnF. Customise the fields in [ ] brackets.

Subject: Request for Full and Final Settlement — [Your Full Name] | Employee ID [XXXX]

Dear [HR Manager’s Name / HR Team],

I hope this email finds you well. My last working day with [Company Name] was [Date], and I am writing to formally request the processing of my Full and Final Settlement.

My details for reference:

I request settlement of the following components as applicable:

I have completed all exit formalities including handover and return of company assets. As per Section 17(2) of the Code on Wages 2019, I request payment of wage components within 2 working days of my last working day.

Please let me know if any additional documents are required.

Warm regards,

[Your Full Name]

[Mobile Number] | [Personal Email ID]

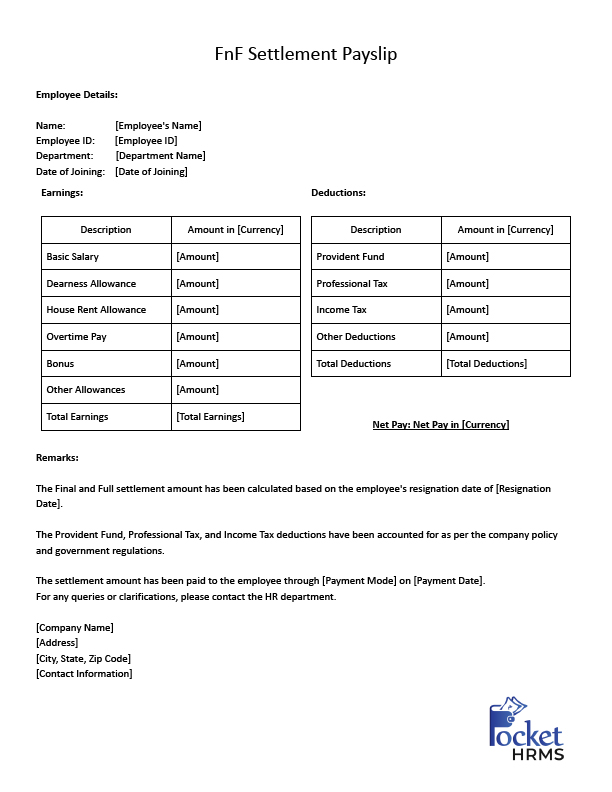

This is the official FnF settlement statement HR issues to the employee. Customise as per your company’s policy.

| Dispute | Root Cause | Prevention |

|---|---|---|

| Notice period recovery dispute | Unclear buyout policy or wrong salary base | Define buyout formula explicitly in offer letter; use gross salary, not CTC |

| Gratuity calculation wrong | Wrong basic salary or service years | Use HRMS that tracks joining date and basic salary from Day 1 |

| Leave encashment disputes | Unclear encashable leave types | Publish clear leave policy; distinguish EL vs SL vs CL encashment rules |

| Payment delayed beyond 2 days | Sequential clearances, manual calculations | Parallel clearance + automated FnF software = the only reliable fix |

| TDS deduction disputes | Wrong slab or exemptions missed | Verify employee’s IT declarations before final TDS computation |

| Asset deduction disputes | No written policy or prior acknowledgement | Maintain signed asset register; include recovery clause in offer letter |

| Gratuity forfeiture disputes | Employer claims misconduct; employee disputes | Forfeiture only valid for Section 4(6) grounds with documented enquiry |

Meeting the 2-day FnF mandate manually is nearly impossible for organisations with more than 30–50 employees — especially when clearances, calculations, and approvals all need to happen simultaneously.

Pocket HRMS’s dedicated FnF module is built specifically for this:

Process FnF settlements in under 2 working days — fully compliant with India’s Labour Codes 2025. Trusted by 1,000+ Indian companies.

Full and final settlement (FnF) is the process of calculating and paying all outstanding financial dues to an employee when they leave an organisation. It covers unpaid salary, leave encashment, gratuity, bonus, and reimbursements — minus deductions like notice period shortfall, loans, and TDS.

FnF full form is Full and Final Settlement. It is also written as F&F, full and final payment, or final settlement. All terms refer to the same process of clearing all financial obligations between employer and employee at exit.

Under India’s new Labour Codes effective November 2025, wage components of FnF must be paid within 2 working days of the last working day — per Section 17(2) of the Code on Wages 2019. Gratuity has a separate 30-day deadline. EPF follows EPFO timelines of 15–20 working days.

FnF includes: pro-rata salary, leave encashment, gratuity (if 5+ years), pending bonus, and reimbursements. Deductions: notice period recovery, outstanding loans, unreturned asset costs, TDS, and professional tax.

Gratuity = (Last drawn Basic + DA) × 15 × Completed years of service ÷ 26.

Eligible for employees with 5+ years of continuous service. Tax-exempt up to Rs. 20 lakhs for non-government employees. Use our FnF calculator above to compute your amount instantly.

Depends on the component. Pro-rata salary, bonus, and notice pay are fully taxable. Gratuity is tax-exempt up to Rs. 20 lakhs. EPF is exempt if service is 5+ years. Leave encashment on resignation is taxable for private sector employees. Leave encashment on retirement is exempt up to Rs. 25 lakhs.

No. Under Section 17(2) of the Code on Wages 2019, paying FnF wage components within 2 working days is a legal obligation. Withholding FnF is a punishable offence. Employees can file a complaint with the state Labour Department.

Send a written email to HR citing Section 17(2), Code on Wages 2019. If unresolved, file a complaint with the Inspector-cum-Facilitator under the Code on Wages at your state Labour Department — labour.gov.in. For gratuity delays, file under the Payment of Gratuity Act 1972.

Employee provides: resignation letter, last 3 salary slips, attendance records, leave balance statement, EPF UAN details, expense claims, bank account details. Employer provides: resignation acceptance, department clearance confirmations, FnF settlement statement.

Yes. All employees — permanent, probationary, contractual, and fixed-term — are entitled to FnF for dues earned. Probation employees may not receive gratuity (if < 5 years) but all other components must be settled.

Under India’s new Labour Codes (effective November 21, 2025), Basic Pay + DA must form at least 50% of an employee’s CTC. Since gratuity and PF are calculated on this “wages” base, a higher basic salary directly increases the gratuity payout in FnF by 25–50% for employees who previously had low basic salary structures. See our 50% Wage Rule section for a full calculation example.

Yes. Under the Code on Social Security 2020 (effective November 2025), fixed-term employees are now eligible for gratuity after just 1 year of continuous service — down from the previous 5-year requirement. The gratuity is calculated proportionately for the period served.